📈 Breaking News: Consumer Debt Soars to All-Time Highs! 📈

📈 Breaking News: Consumer Debt Soars to All-Time Highs! 📈

Americans records are surviving off credit cards. What to know.

Thanks for reading Finessing Finance. As always, your support does not go unrecognized on my journey to help people with free, accessible personal finance content.

Consumer Debt Hits Record Levels

There’s a silent trend happening within the country at this moment. It’s being overlooked and accepted by many people, but I believe this should be the heart of many of our personal finance conversations in 2023. It’s the idea that consumer debt is acceptable and we should be turning to credit cards to support our lifestyles. This is not the case and it’s our duty to educate others in debt.

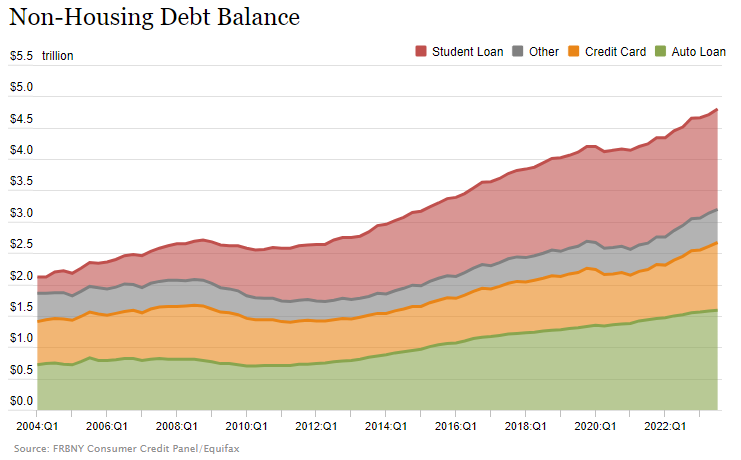

Last week, the Federal Reserve Bank of New York reported that credit card consumer debt has reached a record high of $1.08 trillion dollars.

People may dismiss this news, but it’s important to take note of trends within the country so that we can better predict the future. With this increased load of debt, delinquencies are on the rise as well. People are beginning to default on their debt.

In my personal life, my friends are turning to credit cards to support their lifestyles. One friend recently transferred to a 0% Interest credit card to accommodate for a baby on the way. Another friend turns to debt when it comes to lavishly traveling.

After the pandemic and years of inflation, it’s obvious that this isn’t our fault. We’re tired! We want a break. We want to go and live life, however, this isn’t setting people up for a sustainable long-term future. Many of my peers are worried about climate change, war, famine, and other issues that lead them to spending more than what they’ve earned.

“I think economic inequality is continuing to grow, and that is something that has really accelerated in recent years,” Ted Rossman, senior industry analyst at Bankrate, told CNN.

The History of Consumer Debt

In the United States, the concept of consumer debt has undergone significant transformation over the past century. From a society that predominantly saved for purchases to one where credit cards and loans are ubiquitous, the history of consumer debt in the United States reflects a complex interplay of economic, social, and technological factors.

Early 20th Century: A Thrift-Centric Society

In the early 20th century, the prevailing ethos was one of thrift and savings. People largely abstained from using credit for everyday expenses and instead prioritized saving money to make significant purchases. If a loan was needed, it was typically obtained from a local bank or a friendly neighbor, often for specific and well-defined purposes.

Post-World War II Boom: The Emergence of Consumer Credit

The transformation began in earnest after World War II. The U.S. economy was experiencing unprecedented growth, and this prosperity ushered in the rise of consumer credit. People increasingly started to buy cars, homes, appliances, and other big-ticket items. To facilitate these purchases, the concept of consumer credit began to evolve.

1950s-1960s: The Advent of Credit Cards

The 1950s witnessed the birth of the first credit card, Diners Club, initially designed for dining and entertainment expenses. However, the real game-changer came in 1958 when Bank of America introduced the BankAmericard, a general-purpose credit card that would later become Visa. It revolutionized the way people transacted. They could make purchases on credit, deferring payments until a later date, all without the need to carry cash.

Soon after, other major players like MasterCard and American Express entered the market, further popularizing the use of credit cards. These cards made credit readily accessible and ushered in an era where it became increasingly common to spend money beyond one's immediate means.

1970s-1980s: Deregulation and Easier Credit Access

The 1970s and 1980s saw a shift towards more relaxed regulations on credit. This made it even easier for individuals to obtain credit cards and loans. Consumer debt continued to rise as credit became more readily available.

The 21st Century: A Double-Edged Sword

In the 21st century, consumer debt in the United States remained a significant aspect of everyday life. Credit cards, student loans, car loans, and mortgages all played a role in shaping the financial landscape.

The mid-2000s bore witness to the global financial crisis, triggered in part by a housing market crash. It was a stark reminder of the potential perils of excessive consumer debt, as many individuals found themselves trapped in financial turmoil.

Consumer debt remains a complex issue in the United States today. Some individuals utilize credit wisely, enhancing their financial flexibility, while others struggle with mounting debt. As the history of consumer debt illustrates, while it can be a valuable tool, it demands responsible management to avoid potential pitfalls.

In conclusion, the evolution of consumer debt in the United States reflects the changing dynamics of the American economy and society. It's a story of shifting attitudes, regulations, and technological advancements that have shaped how we interact with and manage personal finances in the modern world. Understanding this history can help individuals make more informed decisions regarding their financial well-being.

How to Tackle Your Debt

I wrote a great article speaking to different methods of tackling your personal debt earlier this year. Check out the below post:

Stay safe out there with your debt and stick to your budget. You’ve got this.

Have a great week,

Jordan