CREDIT SCORES 101

CREDIT SCORES 101

M.B.A., Jordan Jefferys, take on credit

A NOTE FROM THE AUTHOR: Happy 2021! I hope everyone is having a great start to the new year, setting goals, and most importantly, taking steps to accomplish those goals. My goal for this year is to grow this blog and help people with their finances.

This week, I reached out to another Jordan, Jordan Jefferys, to help explain the basics on credit. Jordan and I met in college at Stephen F. Austin State University. She is a whiz on finances and cares as passionately as I do for the world of money. She once advised me on my journey as part of the Rusche College of Business’ Student Advisors!

Let’s make 2021 the best year yet. Here’s Jordan:

Hey there! My name is Jordan Jefferys. I met Jordan Trevino while attending school at Stephen F. Austin State University. We both were tutors at the Academic Assistance and Resource Center, the AARC for short. After leaving the AARC, I joined a program at SFA called the Marleta Chadwick Student Financial Advisors. The goal of the program is promoting financial literacy to East Texas and the SFA community. I worked at this program my last year of undergrad and became the Director while I completed my M.B.A. The Student Financial Advisors allowed me to learn a lot about people and how they perceive finances. One topic that I love getting to talk to people about is credit. Many people are taught that credit is bad, which can be true. In my opinion though, credit is a great when it is used correctly.

Credit Basics

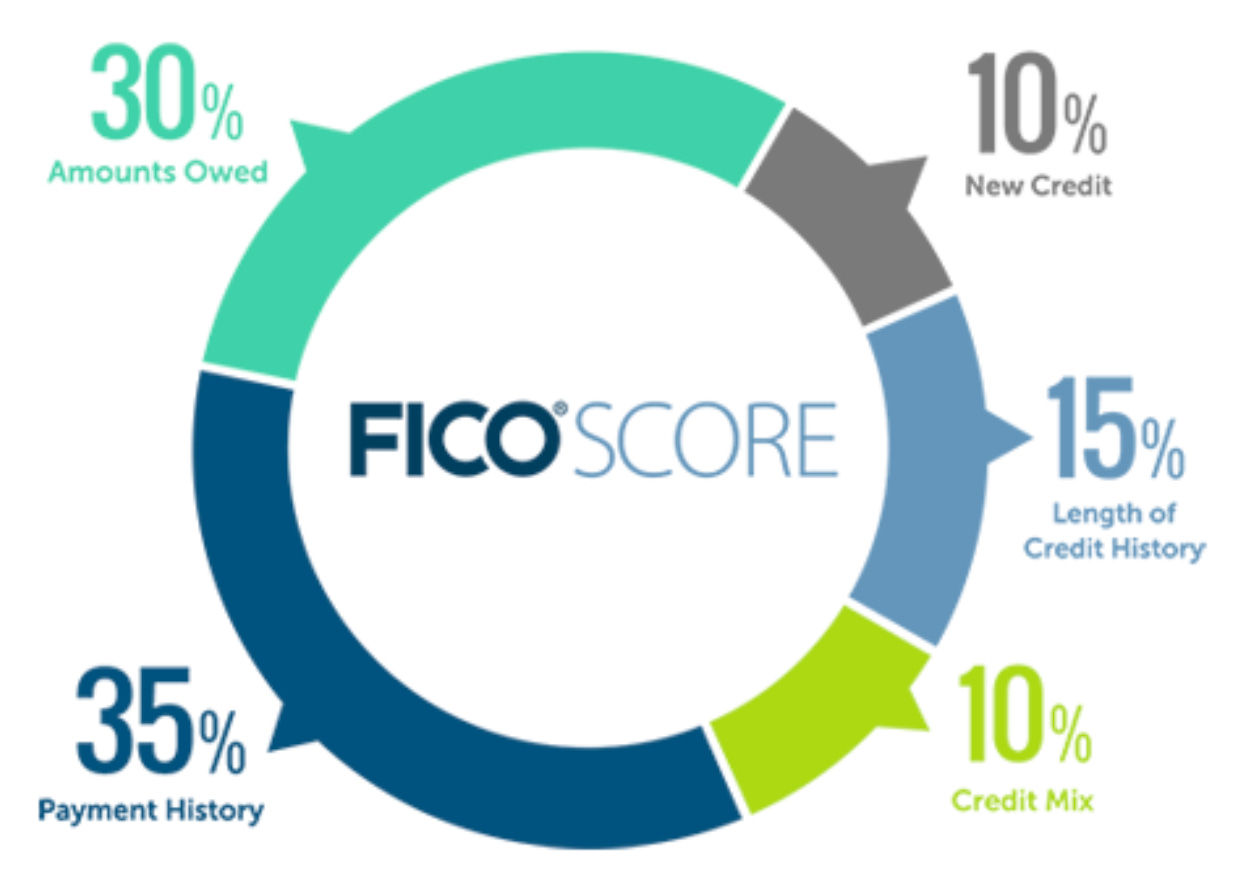

To start, I want to give you some credit basics. My definition of credit is your ability to access goods and services, with the understanding that you will pay for them later. Some examples are credit cards, mortgages, car loans, student loans, etc. Your creditworthiness is determined by your credit score. Here is an illustration on how your credit score is calculated.

Why is this important?

From what I have seen, a lot of people are not worried about their credit score until they are trying to get their first car loan or mortgage. However, it does not help as much as preparing beforehand. I do not want people to fall into this trap. If you plan on making a large purchase (a car using credit, a house, a business, etc.) at any time in your life, I want you to think about your credit sooner rather than later. I say this because lenders make money on your inability to pay or your limited credit history. If you are able to get a loan, it is likely that you will be offered a higher interest rate compared to those with a strong credit history. Your interest rate is important because that is how much money you will be paying to borrow the money. The higher the interest rate, the higher the overall cost for your good or service.

My Story

For me, I started my credit journey in my junior year of college. I applied for a student Capital One Journey credit card. I picked this card because it had no annual fee (it does not cost anything to keep the account open), offering cashback rewards (money I can use that I received from buying items with the card) and there was a higher chance for approval because I did not have a credit history. I was approved with a $500 limit. Since I was a junior in college and never had a credit card before, I thought I was on top of the world. Despite that feeling, I knew this credit card came with a big responsibility. The rule I set for myself was that I would use it if I did not have the money in my bank account to cover the purchases and I would make the full payment each month to ensure that I was not charged interest. I did not want to pay interest because credit cards typically have the highest interest rates of the varying types of credit.

I remember talking with my dad about my credit card a while after I had gotten it. He asked me the interest rate and I told him it was around 23%. He looked at me and said, “THAT IS AWFUL!” It is true that the interest rate on my first credit card was very high, but I had two things to remind myself. It was what I could get with my limited credit history and I was not paying interest. So, as long as I kept to the rule I had set for myself, it was ok that it had a higher interest rate. Since then, I have been able to increase my credit limit. Sometimes credit card companies will increase your credit limit if you are using your credit responsibly and you are able to request a credit limit increase. This is something I do every so often. Looking back, I wish I would have applied for my first credit card sooner. However, I know that I would not have had the same understanding of using a credit card responsibly.

Since then, I have yet to make any large purchases. I am still working to ensure my credit score is as high as it can be. A few years ago, I felt comfortable opening another credit card account. This time it was a Discover It card. I did not need to apply for the student card this time because I had established a credit history for myself. I applied for this card for a few reasons. There was no annual fee, the interest rate was lower than my Capital One card, and the rewards it offers. This card offers a higher percentage of cashback on gas, groceries, and restaurants than my Capital One card. This was important to me because when I looked at my budget, I was spending the most money in those categories. I continue to use the same rules that I set for my first credit card with both of these cards.

My Advice

If you are already exploring options for big purchases, look for options with the lowest fees and lowest interest rates. I encourage you to do your research and do not apply for loans if it does not seem likely for you to get approved. If you are applying for multiple loans and getting denied, it will affect your ability to access credit in the future.

If you are just looking to build your credit I think that a credit card might be the best way to do it, here is what I think you should look for.

Look for credit cards with no annual fees.

This will ensure you are not charged yearly for having your account open. Even if you are not actively using the credit card, you can keep the account open without charge.

Look for credit cards with a lower interest rate.

Always look at the interest rate on the credit card. While I encourage you to pay off the balance every month to ensure you do not have to pay interest, you should always be prepared for the unexpected. If something were to come up and you couldn’t pay, a lower interest rate will ensure you are paying less interest.

Look for credit cards with little or no fees.

Will you be charged fees for paying late, cash advances, foreign transactions, etc.? The lower the fees, the better it is for you.

Look for credit cards that offers rewards that align with your lifestyle.

If you travel often, you might look for a credit card with hotel or flight rewards. If you drive a lot, you might look for a credit card that gives you rewards on gas. Cashback rewards are great, and you can find a credit card that offers different percentages on different items.

There are so many things to learn that fall under the topic of credit, and I am sure Jordan will guide you through that at some point. The one thing I hope you get from me is that credit is very useful. It is just important to use it responsibly.

—

Have a great rest of your week :)

-Jordan T. and Jordan J.