📈Thank You for Your [401K] Contribution📈

📈Thank You for Your [401K] Contribution📈

Focusing on Your 401K Contribution Rate

A WORD FROM THE AUTHOR: At the time of this writing, it’s the day after Elon Musk went live on Saturday Night Live. There was a perfect culmination of factors that played into the -21% price of the cryptocurrency within less than two hours. I remember fear and panic coursing through my mind as I attempted to sell my position of Doge. At the end of the day, I made money. However, I could have made more money if I played logically instead of being greedy.

I want to focus on my latest money move this week regarding my 401K. As always, I am not a financial advisor.

If you’re enjoying this blog, please tell one friend this week! 😀

My Latest 401K Move

This past week, I met with a financial advisor from the Barnum Financial Group over Zoom. I expressed my worries on if I was saving enough for retirement. Over the web call, he stated that contributing to the company match is great but this can leave Americans left out in the long haul as many individuals don’t realize the true cost of retirement.

Before this past week, I allocated 6% of my paycheck to my 401K since 2019. This is match rate typical of most companies and I automatically funneled leftover savings into a Roth IRA. Sounds smart? But there’s an extra step in there.

The Barnum financial advisor recommended I bump my contribution rate to at least 10%. He said that should be the bare minimum that any 401K employee should contribute. He made me realize that allocating 6% will leave you unhappy and wishing you had saved more come time for retirement.

Being the achiever that I am, I actually boosted my 401K contribution to 17%.

Rest In Peace my disposable income.

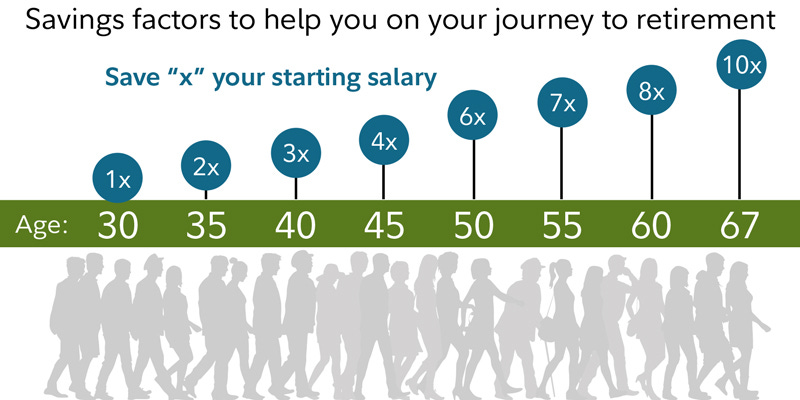

401K Milestones

According to Fidelity from the infographic above, Fidelity recommends you have at least 8x your salary once you reach sixty-years-old. From there, retirement can be based on how much you’ve saved, your means of living in retirement, and when you actually plan to stop working for a paycheck.

Looking at the above graphic, are you on track? Be honest with yourself. If not, you’re not alone. Before this past week, I wasn’t on track either. Contributing to your 401K is the ultimate diamond hands of investing.

Investment Strategy

Many financial gurus maximizing your 401K and contributing the $19,500 yearly limit if possible. If I can handle this reduced monthly income, I plan on seeing if I can push this amount even further to the $19,500. Along with your Roth IRA, you’re contributing a maximum of $25,500 (more or less given your current situation).

The biggest tip here is to maximize these tax-advantaged accounts before investing into Robinhood or crypto where taxes can hit you like a truck. Speaking of taxes, 401K traditional is a tax advantaged account, meaning the percentage you contribute isn’t taxed (and what remains is taxed).

I’m challenging you to evaluate your 401K contributions this week. Are you contributing enough?

Have a great rest of the week,

Jordan