THE STATE OF STUDENT LOANS

THE STATE OF STUDENT LOANS

How the Incoming Administration Impacts Your Student Loans

A WORD FROM THE AUTHOR: As you know, everything has quickly shifted in terms of finance this week and I’m going to do my best on reporting the latest changes within the Biden administration that impact you surrounding student loans. I hope this issue updates you on the latest and helps you tackle any student debt.

As always, please share this article with your friends to help support the cause!

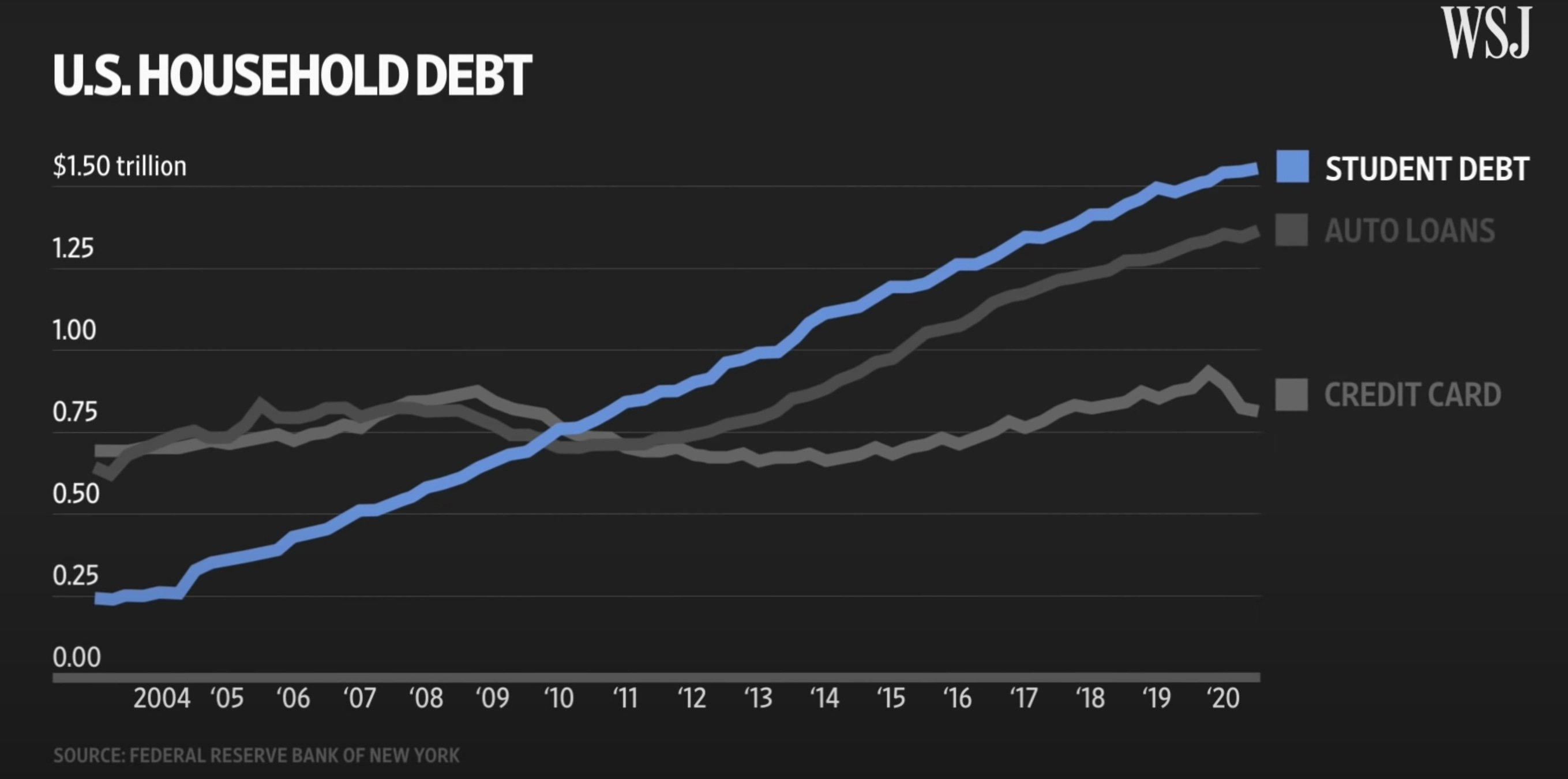

Background

Wall Street Journal reports that in December 2020, there is a $1.6 Trillion outstanding student loan debt within the United States. That’s a meteoric rise of the quarter of a trillion since 2004. It’s widely agreed upon that the cost of college is increasing at a sharp rate, and this isn’t due to your university’s luxury dormitories but cost-of-living for employees and federal funding cuts to higher education.

Off-setting the cost of higher learning to students is placing scholars in a disadvantaged position for succeeding after graduation. The chance of making over six figures out of college is slim and paying down student loan debt is removing chunks of your potential wealth journey.

One topic to consider is who is reaping the rewards of the currently proposed $10K forgiveness. The Brookings Institution reports that 60% of student debt is owed by people in upper-income households.

Forgiveness

From the latest news, the administration is seeking to forgive up to $10K in federal student loans. This has been a topic of debate from the amount to forgive and if we should forgive in the first place.

Federal student loans went on pause last year with the interest rate diminishing to 0% and flexibility in skipping payments. The latest news says this executive order has been extended to September 2021. We’ve gone an entire year without being mandated to pay our student loan debt. This flexibility is helping

If you’re waiting on forgiveness, Dave Ramsey says you shouldn’t be waiting in the first place. He says that you should pay the debt off as aggressively as you can and seek financial freedom without waiting on the government.

The $10K will need to be approved by the latest congress before we see any implementation to our overall bill.

My Personal Story

When student loans went on pause last year, I knew I needed to strategize a plan to maximize this opportunity. Before then, I was aggressively paying down student loan debt with every leftover penny outside my emergency savings built up. When the current 0% interest was implemented, I knew I had the greatest asset of all on my side, time.

I made an oath to myself that I wouldn’t pay my student loans until forced. With the leftover savings at the end of each month from not having to pay the bill, I invested heavily in the stock market when the market was at its lowest.

From there, I made my money work for me and nearly doubled the amount I had originally invested. Meaning, I’m currently in a position to pay off my student loans in full because I took leftover money and sought to maximize returns.

My next plan of attack is to continue this strategy until payments resume.

Don’t let your money sit around. Your money should work for you.

Actionable Advice

My personal recommendation is to wait until student loans are mandated again in September and invest your money to seek the maximum amount of returns.

Seek the most affordable tuition if you’re in a position of going back to school.

Aggressively attack student loan debt. The compounding interest will sneak up on you, robbing you of thousands of dollars for no reason.

Have a great week :)

-Jordan